Industrial emissions

Buyers need to know that a tonne of carbon claimed as removed was truly removed and that it will stay removed.

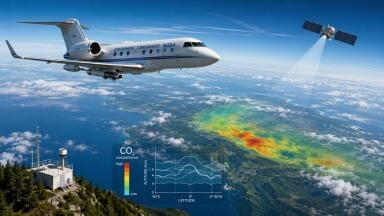

As Europe finalises its Carbon Removals Certification Framework (CRCF), that confidence will increasingly rest on the ability of satellites and sensors to measure, verify, and audit carbon fluxes across millions of hectares.

At the 3rd Forum on Earth Observation for Carbon Markets, policymakers, scientists, and market actors grappled with a simple but profound question.

Can we build a carbon market credible enough to scale?

The CRCF is the EU’s attempt to bring order to the chaotic world of carbon removals.

It aims to define what qualifies as a genuine carbon removal, how permanence is proven, and how certification interacts with national climate targets.

Earth observation is integral to this plan.

From afforestation and rewilding to regenerative agriculture, EO data can help quantify baseline carbon stocks, track changes over time, and detect reversals such as wildfires or land conversion.

But between those capabilities and a tradable carbon credit lies a maze of methodological, economic and ethical challenges.

For EO to support carbon credits, it must do more than measure change, it must estimate what would have happened otherwise.

This counterfactual baseline is notoriously difficult to pin down, particularly in dynamic landscapes where weather, management and market conditions fluctuate.

Satellites can detect a greener field or a denser canopy, but without context, they can’t determine causality.

That means EO needs to be combined with field data, management records and modelling to establish credible baselines.

How that integration happens and who certifies it remains one of the thorniest debates in carbon accounting.

Even with good data, verification is a hurdle.

Market participants and auditors need confidence in both the algorithms and the data pipelines used to generate carbon estimates.

If models are proprietary or opaque, verification becomes faith-based.

Transparency will therefore become a currency in its own right: open algorithms, documented uncertainty, and reproducible workflows could become prerequisites for CRCF certification.

Yet, paradoxically, the more transparent the system, the easier it is for bad actors to mimic it without substance.

The Forum will likely explore how to balance open science with fraud prevention, perhaps through blockchain-style audit trails or digital MRV platforms that lock data provenance.

Verification is expensive, and many voluntary projects barely break even once transaction costs are included.

EO promises to reduce those costs by automating monitoring, but satellites are not free, nor is the analytics expertise needed to interpret them.

Economies of scale may help: shared EO infrastructures, standardised methods, and pooled baselines could spread costs across many projects.

The EU hopes CRCF will catalyse this standardisation, giving smaller landowners and farmers access to verification tools that previously only large developers could afford.

Still, there’s a risk of centralisation.

If verification becomes the preserve of a few EO service providers, market diversity and trust could suffer.

The CRCF doesn’t operate in a vacuum. Credits certified under its framework must align with Member States’ greenhouse gas inventories and the EU’s LULUCF accounting, or risk double counting.

Here again, EO plays a bridging role.

Satellites can help detect leakage (where emissions are displaced elsewhere) and provide a common evidentiary basis between voluntary and compliance regimes.

But the more the two systems intertwine, the higher the stakes: a data error in a voluntary project could ripple into official climate accounting.

If the CRCF succeeds, EO-backed credits could become a premium product; auditable, comparable, and perhaps even tradable across jurisdictions.

But that credibility will come with strings attached: continuous monitoring, rigorous uncertainty quantification, and periodic recalibration.

For project developers, this may mean smaller but more secure margins.

For buyers, it could mean paying more for verified integrity.

The market’s next challenge will be psychological as much as technical: will investors accept fewer, slower credits if they trust them more?

As the Forum convenes, expect discussion to turn from data to governance. The crucial questions are no longer just scientific, but political.

The next generation of carbon markets will be shaped by EO specialists, regulators and auditors.

For environmental monitoring professionals, this is a call to redefine the instrumentation of trust.

The satellites are ready. The question now is whether the market is.

IET 36.3 May

.jpg)